Backtesting Your Portfolio

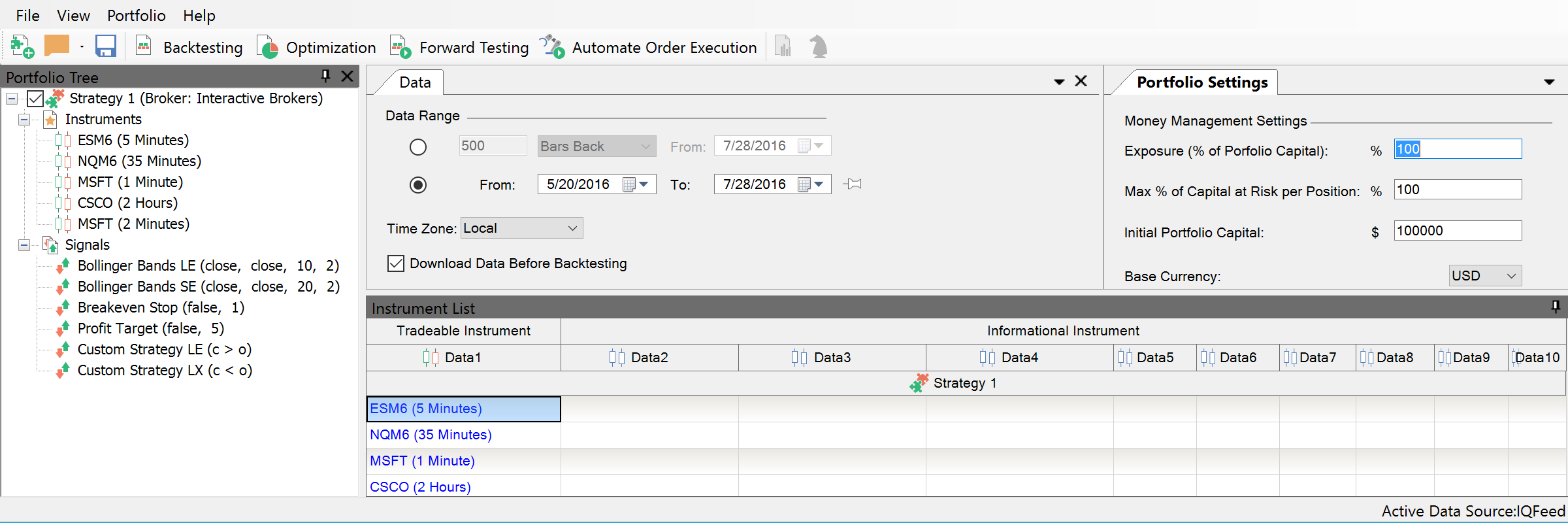

Portfolio backtesting means applying one or more strategies to many instruments at once — simulating on historical data and gauging performance as if all symbols were traded with these strategies. Different symbols can even have different resolutions during the testing: 1 tick, 3 minutes, 9 days or others. MultiCharts 64 bit version is essential for portfolio backtesting as it's very easy to reach critical mass with the huge number of combinations. For technical information on this feature look at the related Wiki page.

Portfolio Trader

Real-life constraints considered

Considering real-life constraints is critical for creating successful portfolio trading strategies. During portfolio backtesting, trading signals often need to be prioritized because there is not enough money in the account to place all orders. Your strategy might always buy the cheapest instruments first, or you might want it to always fill stock orders before futures orders.

Define money management within scripts

Money management options can be easily changed through the Portfolio Trader interface or by directly using PowerLanguage code. We have added the Portfolio Money Management keywords at your convenience. Please note that all keywords returning or receiving money values are using the currency specified in the Portfolio settings. Learn more technical info on our Wiki page.

Optimize your portfolio in a couple of clicks

Portfolio optimization lets you find optimal parameters for each of your portfolio strategies —one at a time or all at once. Both exhaustive and genetic optimization methods are available in the portfolio backtesting engine. The 64-bit version of MultiCharts handles huge data needed for both tasks with ease.

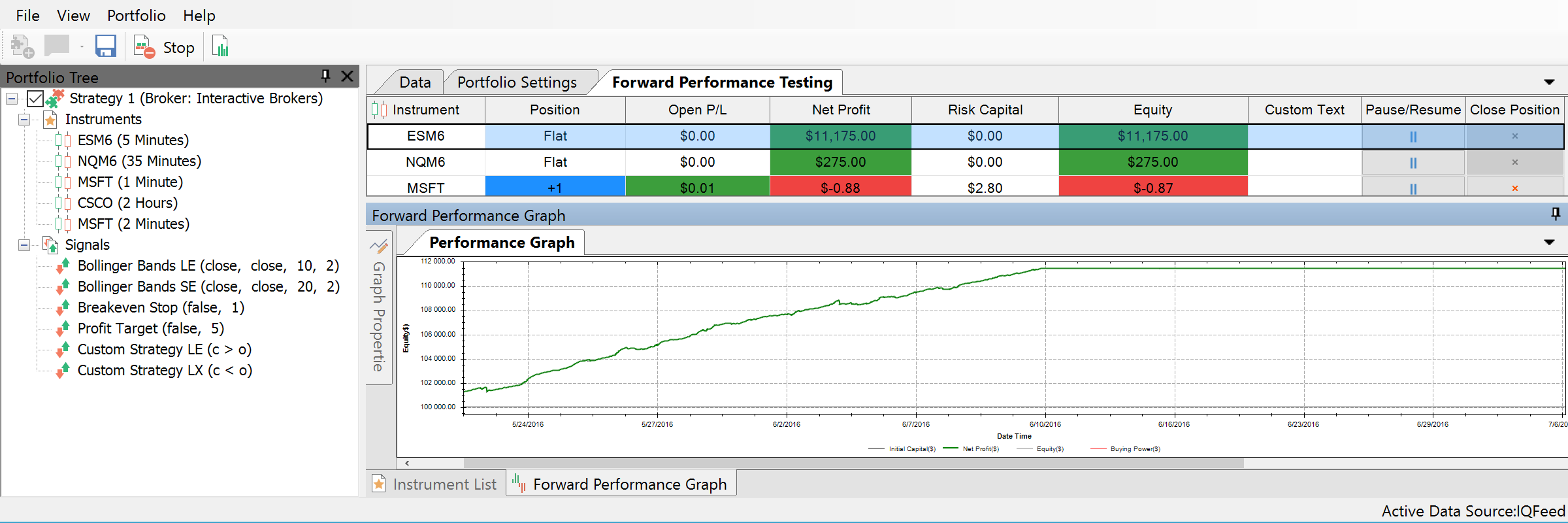

Forward Testing

The process of testing a trading strategy in real-time, but without actual trading at broker. A trader can do a simulation of his or her trading strategy on relevant data in order to gauge its effectiveness. At your convenience the Forward Performance Testing window contains the main information on strategy performance for every instrument.

Portfolio Trader

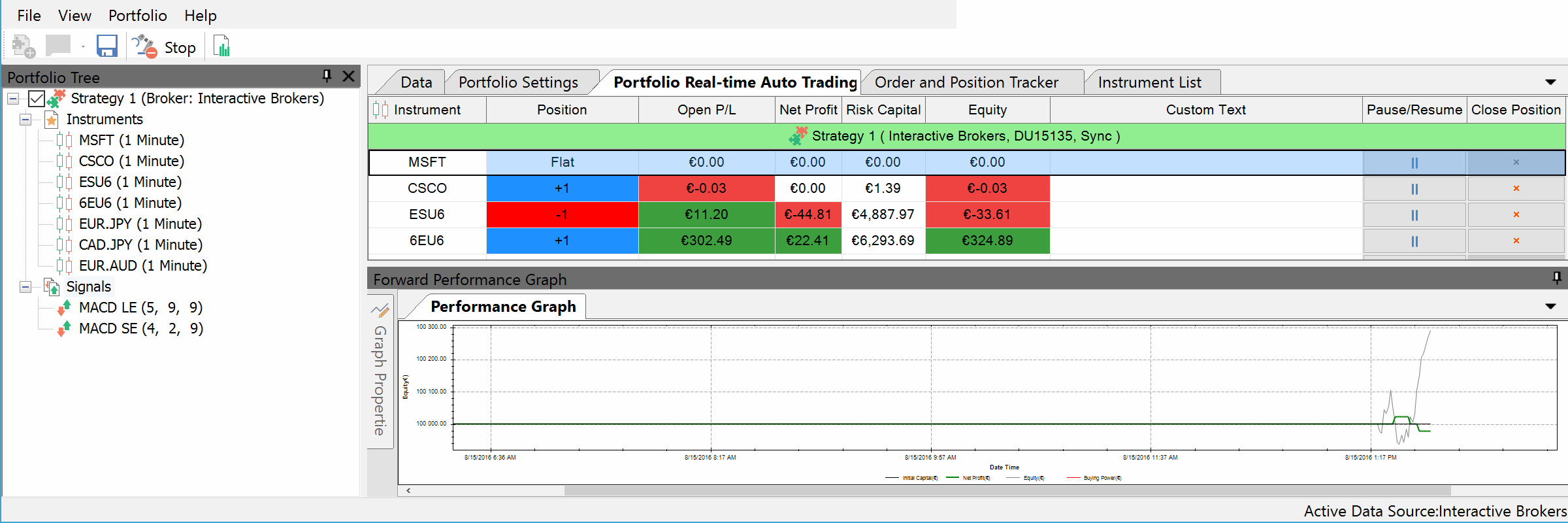

Portfolio Automated Trading

MultiCharts Portfolio Trader can process multiple strategies applied on different groups of symbols and route orders to various brokers. After backtesting and optimizing the strategies, you can switch to real trading when orders are sent to the broker. Also, you can pause and resume the trading on any of the instruments whenever you need just in one click.

Portfolio Trader

Use more than one strategy at a time

Portfolio Trader is very flexible in letting you create several strategies and combine them in many ways. Symbols can be divided into groups and each group can have its own strategy. For example, you can have “Rotation” and “Spread” strategies applied to different groups of instruments in your portfolio. Also, you can have one trading system that trades stocks and another that trades futures. The performance of each strategy will impact your overall portfolio performance. See Portfolio Trader strategy examples here.

All trading details at your fingertips

Order and Position Tracker is available during autotrading process so you can check your account balance or Open P/L at any time just in one click. It provides detailed summary of orders, positions and accounts across all brokers being used for trading. You can cancel or modify pending orders, or even flatten entire positions, directly from this window.

Interactive portfolio performance report

MultiCharts’ portfolio report is an essential tool when evaluating how your strategies are doing. It is just like our regular performance report, but it features the ability to view breakdown by symbols or show a correlation matrix. Portfolio Performance Report is available in Auto Trading Mode. It shows results generated from the moment it was opened.

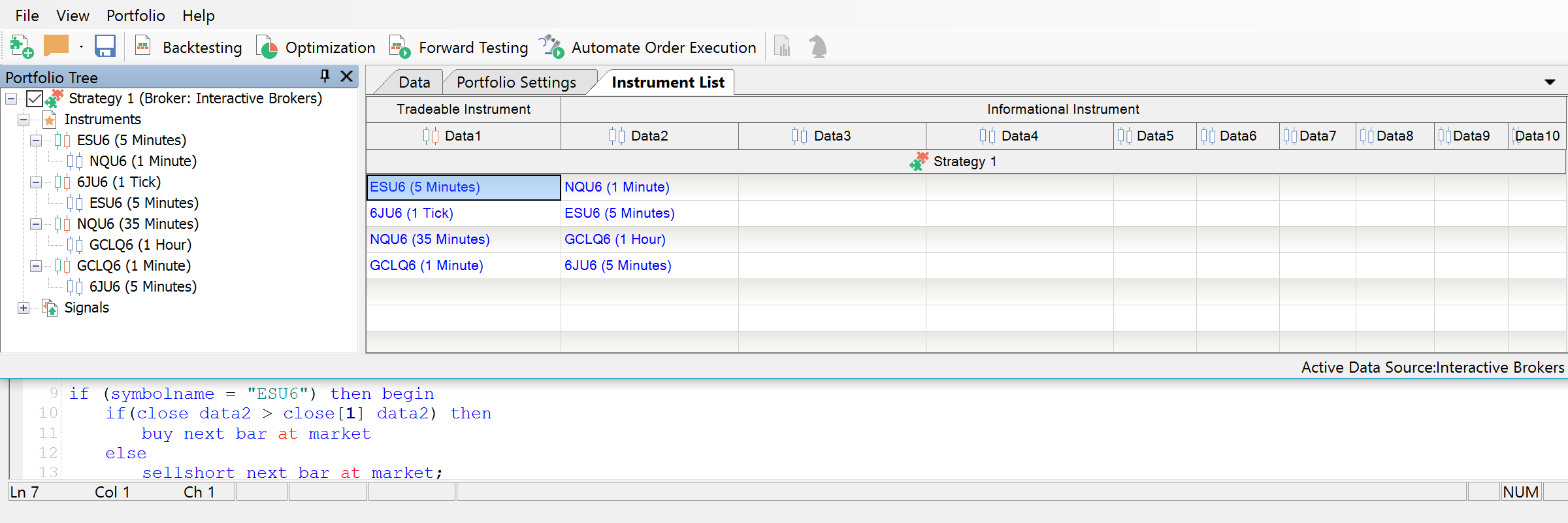

Reference other instruments with ease

Your trading strategy can reference up to nine other instruments in order to make a trading decision on any tradable symbol. This opens new opportunities of testing strategies such as statistical arbitrage or pair trading. Let’s consider a pair trading strategy. When one of the pair is bought or sold, your strategy needs to know exactly what’s going on with both symbols. If your pair is Google and Microsoft, you would enter GOOG as symbol one and MSFT as symbol two. Then you would add MSFT as data one and GOOG as data two. This way each instrument in the pair is actively referencing the other instrument—and you achieve complete synchronization.

Portfolio Trader