Backtest on Bid/Ask data?

-

TJ

- Posts: 7742

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2222 times

Re: Backtest on Bid/Ask data?

- Attachments

-

- backtest_bidask.jpg

- backtest_bidask

- (39.29 KiB) Downloaded 2381 times

-

glen demarco

- Posts: 35

- Joined: 16 Nov 2009

- Contact:

-

wullenweber helmut

- Posts: 60

- Joined: 21 Dec 2007

- Has thanked: 3 times

- Been thanked: 9 times

Limit order touched

Using the classic mode of backtesting, without bid-ask-data, a feature to set different slippage parameters for the entry and the exit would be helpful.

Lets assume, a trader is entering the market on stop at 2900 (with no slippage) and wants to sell with limit 2910. If the price of 2910 is touched, Multicharts counts this trade as a winning one.

The more realistic view is, to count this trade as a winner not before the price reached 2911, to be sure that the order would have been filled.

My idea of coding this:

If buy condition is true then buy next bar at 2900 limit;

If marketposition = 1 sell next bar at 2911 limit;

Using a feature setting the parameter for slippage by entry = 0 and setting the parameter for slippage by exit = 1.

Resulting a trade with 10 ticks profit in the trade report.

Lets assume, a trader is entering the market on stop at 2900 (with no slippage) and wants to sell with limit 2910. If the price of 2910 is touched, Multicharts counts this trade as a winning one.

The more realistic view is, to count this trade as a winner not before the price reached 2911, to be sure that the order would have been filled.

My idea of coding this:

If buy condition is true then buy next bar at 2900 limit;

If marketposition = 1 sell next bar at 2911 limit;

Using a feature setting the parameter for slippage by entry = 0 and setting the parameter for slippage by exit = 1.

Resulting a trade with 10 ticks profit in the trade report.

-

TJ

- Posts: 7742

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2222 times

-

wullenweber helmut

- Posts: 60

- Joined: 21 Dec 2007

- Has thanked: 3 times

- Been thanked: 9 times

-

Rick Webber

- Posts: 50

- Joined: 04 Jan 2008

- Has thanked: 21 times

- Been thanked: 3 times

-

TJ

- Posts: 7742

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2222 times

Can someone give a code example say to"BuytoCover next bar at 1068.25 limit"and "Sell next bar at 1068.25 limit" using the Bid/Ask capabilities in this topic.Thks.

There is no change to the code.

(remember: this is the backtest of a code !)

the only difference is the application of data:

in a normal Classic Backtesting, you use one data stream -- the consummated trade price at specific time intervals.

in an Extended Backtesting (bid/ask),

you apply 2 data streams to the chart.

with the first data stream, you assign the ask price to the Quote Field,

and

with the second data stream, you assign the bid price to the Quote Field.

- Attachments

-

- bid_ask.jpg

- bid ask

- (37.91 KiB) Downloaded 2248 times

Last edited by TJ on 17 Nov 2009, edited 1 time in total.

-

TJ

- Posts: 7742

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2222 times

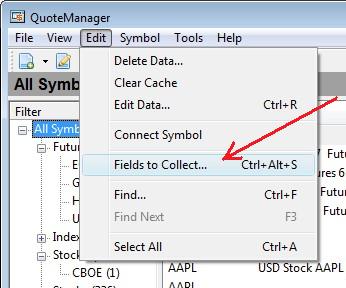

Bear in mind... if you want to do Extended Backtesting using Bid/Ask prices,

you will need to collect the data ahead of time.

you will need to collect the data ahead of time.

- Attachments

-

- Fields_to_Collect.jpg

- Fields to Collect

- (16.05 KiB) Downloaded 2345 times

-

- QM.jpg

- QuoteManager

- (21.6 KiB) Downloaded 2334 times

-

Rick Webber

- Posts: 50

- Joined: 04 Jan 2008

- Has thanked: 21 times

- Been thanked: 3 times

-

JoshM

- Posts: 2195

- Joined: 20 May 2011

- Location: The Netherlands

- Has thanked: 1544 times

- Been thanked: 1565 times

- Contact:

Re: Limit order touched

I'm wondering how someone would estimate the slippage, if any, when using the bid/ask data when backtesting?Using the classic mode of backtesting, without bid-ask-data, a feature to set different slippage parameters for the entry and the exit would be helpful.

In the MultiCharts manual, page 206, I found the following description:

I have not a lot of experiencing with translating backtested strategies to real-time trading conditions (i.e. how a backtested strategy will perform in real-time), so I'm wondering what slippage (if any) penalty would be required when using Precise Back Testing. As I read it, the manual suggests that slippage settings are not needed, but I rather be pessimistic in my assumptions so I'm wondering:With Precise Back Testing, the user can load the historical bid data series and the historical ask data series into MultiCharts. MultiCharts will use the ask data series to fill buy market orders and buy stop orders. Similarly, MultiCharts will use the bid data series to fill sell market orders and sell stop orders.

Should I use the normal slippage settings or would that give an extra penalty because the bid/ask data is already incorporated in the spread? Perhaps I can use smaller slippage with Precise Back Testing (say, an half to 3/4 of regular?)

Or should I maintain the regular slippage and use the Precise Back Testing more for testing if there's enough liquidity?

Can someone, support or other users, comment on this?

Thanks in advance,

Josh

-

Stan Bokov

- Posts: 963

- Joined: 18 Dec 2009

- Has thanked: 367 times

- Been thanked: 302 times

Re: Backtest on Bid/Ask data?

Well, logically 'slippage' means the difference between the price you expect to get filled at and the price you actually get filled at.

If you are doing standard backtesting using Trade prices, and your strategy performs well, you may be expecting to receive similar performance during real-time (innately assuming that fills will happen at prices similar to Trade prices). However, in real-time you get filled at Ask and Bid, which increases the slippage, and thus makes your backtesting look overly optimistic.

Most traders would rather avoid overly optimistic backtesting, and bring it as close to real-time as possible. Using Bid/Ask series for backtesting will give you more realistic fill prices in the past, and probably bring down the performance of your strategy. This brings it more in line with real-time, and reduces your slippage. However, some slippage factors remain (long fill times, internet disconnects, etc).

I would still assume the worst and keep slippage close to normal, whatever that 'normal' is. Just my two cents.

If you are doing standard backtesting using Trade prices, and your strategy performs well, you may be expecting to receive similar performance during real-time (innately assuming that fills will happen at prices similar to Trade prices). However, in real-time you get filled at Ask and Bid, which increases the slippage, and thus makes your backtesting look overly optimistic.

Most traders would rather avoid overly optimistic backtesting, and bring it as close to real-time as possible. Using Bid/Ask series for backtesting will give you more realistic fill prices in the past, and probably bring down the performance of your strategy. This brings it more in line with real-time, and reduces your slippage. However, some slippage factors remain (long fill times, internet disconnects, etc).

I would still assume the worst and keep slippage close to normal, whatever that 'normal' is. Just my two cents.

-

khalaad

- Posts: 323

- Joined: 07 Jan 2007

- Location: Lahore, Pakistan

- Has thanked: 64 times

- Been thanked: 57 times

Re: Backtest on Bid/Ask data?

Sensible, Stan.I would still assume the worst...

I am a discretionary, not systemic, trader. But in recent I have done a bit of research on systematic trading and my finding is slippage should be factored in at 3 times the average spread when running standard back-testing using TRADE prices to adequately factor for the spread, latency, the un-known, etc.!

This way there are fewer forward-testing surprises.