Essential tool for robust systems

The essence and the main advantage of Walk-Forward testing is that it combines optimization and backtesting. During the process, optimal inputs are tested against real market conditions to see how they would perform. Multiple WFO tests help to prove or disprove the validity of your trading system. The idea behind walk-forward testing is illustrated below:

Technical details of the process

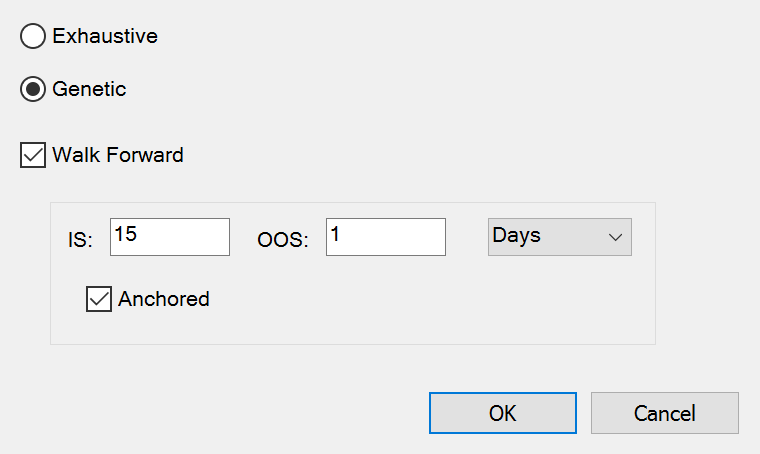

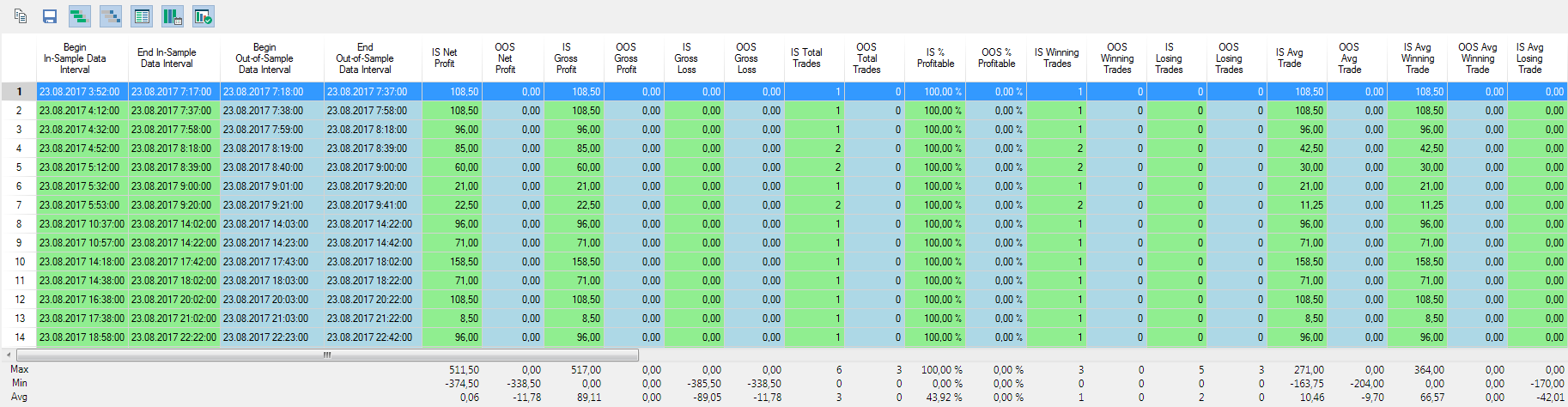

Walk Forward Optimization segregates the data series into multiple segments, and each segment is divided into an in-sample (IS) portion and an out-of-sample (OOS) portion. Parameter optimization for the strategy is performed using the IS portion of the first segment. The same parameters are then used to back test the strategy on the OOS portion of the same segment. The process is repeated for the remaining segments. The OOS performance results from each of the segments are considered "real" instead of "curve-fit" because the parameters that produced the OOS results were generated from IS data.

Preventing curve fitting

The entire data series is broken up into smaller parts. A series of tests is done, and each test is done on a small portion of the whole data series (in-sample data). When optimal input values are found for that small portion, the software checks how they would have performed in the real world by applying them to data that was not part of the test (out-of-sample data). The tests continue to repeat until you have tested the entire data range. In the end, you are shown the results that performed the best under varying market conditions. This helps prevent over-optimization, also known as ‘curve-fitting’.

Different options to suit your needs

Depending on a trader’s tasks, Walk-Forward testing can be used with both exhaustive and genetic optimization methods. You can specify different sizes for your in-sample and out-of- sample data, and you can even display information in bars or days. Walk-Forward analysis adds more accuracy and detailed optimization. It’s a real stress testing for your trading strategy.

No jumping forward

There is also a modification to the walk-forward process, called the anchored mode. When you select the anchored mode, the in-sample data stays anchored to the beginning and gets longer for each test, instead of jumping forward. This is another way of making sure your results are robust.

Select Optimization Method

Walk-Forward Optimization Report

Export to Excel with one click

The walk-forward testing report can be exported to Excel with just one click. Then you can perform additional analysis on the data you found during the test.