Hi,

I'm noticing that it is often taking at least a second and on occassions nearer two seconds to get an order to market from the time the calculation is initiated.

I use MC64 with Patsystems as my broker and IQ feed as my data vendor.

I run about 17 live charts which on average run with about 5k bars history, 1 signal and about 3 indicators (all simple code) each.

My hardware: AMD phenom II x4 850 3.3ghz, 4gb Ram, windows 7 64bit.

Please share you experiences as I have no idea if this is normal for Multicharts64/my setup.

What has specifically made me submit this post is the following:

Last night for the open of Nymex's CL, the first tick triggered my signal to calculate and submit a buy limit order above market (as intended). Unfortunately, I had a lag of at least 1.015 seconds meaning I missed the fill. Sod's law, this missed trade went straight to my target 44 minutes later in pretty much a straight line. The order tracker states that the order was submitted 2 seconds after the opening time of 2300gmt. The time betwen the first tick following the opening time and the tick where my limit order price was exceeded (and never touched again) was 1.015 seconds.

Please let me know your thoughts.

Specifically, is it:

A) Multicharts and/or powerlanguage are not capable of lower latency times

B) My computer is too slow.

C) Its Pats API/Plugin related.

Many thanks,

Will

Latency. Please share experiences.

Latency. Please share experiences.

- Attachments

-

- CL tick chart annotated.PNG

- CL tick chart annotated

- (47 KiB) Downloaded 6913 times

-

TJ

- Posts: 7752

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2228 times

Re: Latency / slow order submission. Please share experience

My first thought is...

4GB is not a lot of memory these days, especially for a trading computer with 17 charts.

Please make a screenshot of your TaskManager Performance tab. It should tell you if your memory utilization is ok.

The CPU, though not a fast one, should be adequate. Again, the TaskManager should give you the indication if you are overloaded.

This chart will show you where your CPU stands in relation to the current offerings:

http://www.cpubenchmark.net/cpu_list.php

4GB is not a lot of memory these days, especially for a trading computer with 17 charts.

Please make a screenshot of your TaskManager Performance tab. It should tell you if your memory utilization is ok.

The CPU, though not a fast one, should be adequate. Again, the TaskManager should give you the indication if you are overloaded.

This chart will show you where your CPU stands in relation to the current offerings:

http://www.cpubenchmark.net/cpu_list.php

Re: Latency / slow order submission. Please share experience

Hi TJ,

Please find attached my task manager.

So from your response, you think that the latency I'm experiencing is indeed excessive (calculation to order hitting exchange)?

I suspect I'm near the limit to whats advisable, performance wise, and am awaiting a move onto a server. But when I say near the limit would you agree that the spare capacity that you can see on my task manager should be okay (or not)?

Thanks.

Please find attached my task manager.

So from your response, you think that the latency I'm experiencing is indeed excessive (calculation to order hitting exchange)?

I suspect I'm near the limit to whats advisable, performance wise, and am awaiting a move onto a server. But when I say near the limit would you agree that the spare capacity that you can see on my task manager should be okay (or not)?

Thanks.

- Attachments

-

- TM snip.PNG

- Task manager image

- (43.79 KiB) Downloaded 6925 times

-

TJ

- Posts: 7752

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2228 times

Re: Latency / slow order submission. Please share experience

My response was my first thoughts only... the computer spec caught my eyes, I did not have time to study your other data.Hi TJ,

Please find attached my task manager.

So from your response, you think that the latency I'm experiencing is indeed excessive (calculation to order hitting exchange)?

I suspect I'm near the limit to whats advisable, performance wise, and am awaiting a move onto a server. But when I say near the limit would you agree that the spare capacity that you can see on my task manager should be okay (or not)?

Thanks.

The opening is always a kaotic time. One second at the opening is not a lot of time, and I do not know what kind of internet latency you have, and how accurate is your computer clock compared with the exchange time.

It is difficult to tell the exact cause of events from your chart; I would gather the logs (both from MultiCharts and your broker) and use Live Chat to let tech support check your system out.

Re: Latency / slow order submission. Please share experience

Thanks TJ.

I trade from a prop firm in London so our internet bandwidth (especially on a Sunday evening) is good.

Unfortunately I had logs disabled as I was troubleshooting another issue I was having with MC.

As you say, I suspect the high load of the market opening might be the cause of a small lag. I'll start monitoring the latency for intraday order submissions.

If anyone wants to share their experience/knowledge of latency with what they think are typical/acceptable times taken from calculation till order hitting the exchange, I would be very interested to hear.

I trade from a prop firm in London so our internet bandwidth (especially on a Sunday evening) is good.

Unfortunately I had logs disabled as I was troubleshooting another issue I was having with MC.

As you say, I suspect the high load of the market opening might be the cause of a small lag. I'll start monitoring the latency for intraday order submissions.

If anyone wants to share their experience/knowledge of latency with what they think are typical/acceptable times taken from calculation till order hitting the exchange, I would be very interested to hear.

Re: Latency / slow order submission. Please share experience

escamillo, I hope that is the case as it's easily rectified.

Would you care to elaborate. What are you running and with what latency or with what spare capacity? Or how was such a conclusion so obvious to you?

Thanks.

Would you care to elaborate. What are you running and with what latency or with what spare capacity? Or how was such a conclusion so obvious to you?

Thanks.

Re: Latency / slow order submission. Please share experience

1 full second is extremely bad latency. MC should process your orders within a few microseconds on your side of things. Although its the easiest to blame, I doubt its your machine. Your connection is almost always the issue.

1. Download PingPlotter to your trading machine

2. Find the relevant IPs for IQ and Pats

3. Do a round trip ping test to IQ feeds servers (my average is 2ms)

4. Do a round trip ping test to Pats Order servers (my average is 2ms)

5. Add that up and double it for good measure

I'd love to hear from the MC team on this as well. I'm curious how "fast" this software is.

1. Download PingPlotter to your trading machine

2. Find the relevant IPs for IQ and Pats

3. Do a round trip ping test to IQ feeds servers (my average is 2ms)

4. Do a round trip ping test to Pats Order servers (my average is 2ms)

5. Add that up and double it for good measure

I'd love to hear from the MC team on this as well. I'm curious how "fast" this software is.

Re: Latency / slow order submission. Please share experience

Great thanks MAtricks, very useful. I'll start investigating that now and post the results here.

Additionally:

My computer clock is 4 secs fast.....could that be an issue?

I use IQfeed for the calculation of my signals which are submitted to Pats. Could not using Pats as the basis for calculation be an issue and a possible cause of latency? I use the former setup and I find IQ the smoother and more reliable of the two.

Additionally:

My computer clock is 4 secs fast.....could that be an issue?

I use IQfeed for the calculation of my signals which are submitted to Pats. Could not using Pats as the basis for calculation be an issue and a possible cause of latency? I use the former setup and I find IQ the smoother and more reliable of the two.

Re: Latency / slow order submission. Please share experience

3rd party anything adds another trip to the process, but it won't be more than a few milliseconds.. Unless you're attempting low latency projects which should not be attempted with MC, this won't be an issue.

Your pc clock shouldn't matter unless your signals are triggered on a time of day event.

Your pc clock shouldn't matter unless your signals are triggered on a time of day event.

-

TJ

- Posts: 7752

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2228 times

Re: Latency / slow order submission. Please share experience

It matters in the first second of the trading session.::

Your pc clock shouldn't matter unless your signals are triggered on a time of day event.

Re: Latency / slow order submission. Please share experience

I'd love some help from MC.

Maybe some hyperlinks to other threads.

My computer clock is now in synch with exchange time. I'm noticing that "generated" order column in the tracker is showing 1-2 seconds post the turn of time intervals for the submission of orders.

Would anyone else out there care to check their order and position tracker and report back with the seconds passed a given time interval that your orders are submitted. Would be very helpful indeed.

Also, in TS you can use to measure code calc speed:

What might be the equivalent in Multicharts (down to milliseconds)? Is there a stopwatch / milliseconds DLL timer type thing I can use?

Thanks!

Maybe some hyperlinks to other threads.

My computer clock is now in synch with exchange time. I'm noticing that "generated" order column in the tracker is showing 1-2 seconds post the turn of time intervals for the submission of orders.

Would anyone else out there care to check their order and position tracker and report back with the seconds passed a given time interval that your orders are submitted. Would be very helpful indeed.

Also, in TS you can use to measure code calc speed:

Code: Select all

inputs:

TimerON(true);

{ Components declaration }

var:

elsystem.StopWatch StopWatch1( NULL ),

intrabarpersist double StrategyTime(0);

{ This method gets called by EasyLanguage one time at the beginning to create and initialize the components }

Method override void InitializeComponent()

begin

StopWatch1 = new elsystem.StopWatch;

StopWatch1.Start();

end;

if LastBarOnChart then begin

If TimerON then begin

StrategyTime = StopWatch1.ElapsedMilliseconds/1000;

print("Strategy Time = ", StrategyTime:14:3, " Sec Bars Analyzed = ", BarNumber:11:0);

end;

end; Thanks!

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency / slow order submission. Please share experience

Dear users,

In general case:

Once the order is generated in MultiCharts with certain parameters – it is sent to the broker. The broker processes the order and fills it or rejects it. The broker is in charge of order execution price, time and order status report. MultiCharts waits for the order status from the broker to show it in MultiCharts. If any modification or cancel command is generated by the code in MultiCharts – it is sent to the broker.

Usually such commands are generated and processed in MultiCharts within milliseconds.

From MultiCharts logs we can measure the time from generating the command and sending it outside of MultiCharts (broker API), and the time from receiving the reply command outside of MultiCharts (broker API) until processing it and displaying the status in MultiCharts interface. MultiCharts cannot affect the possible Internet latency and/or the broker order processing speed, as well as the broker sending the order status.

Order and Position tracker shows local PC time. Some millisecond delay is possible between MultiCharts receiving the order status and processing it, showing it on the OPT window.

Wilkinsw, as for the your particular case, as we have already discussed in the email correspondence, please send me the MultiCharts logs and OPT tabs export so that we can study them and provide the analysis: how long did it take to generate the order in MultiCharts, process it and send the order command to the broker, when did the broker provide the order status reply.

I will ask our developers if that is possible to create a code for measuring the code calculation speed.

In general case:

Once the order is generated in MultiCharts with certain parameters – it is sent to the broker. The broker processes the order and fills it or rejects it. The broker is in charge of order execution price, time and order status report. MultiCharts waits for the order status from the broker to show it in MultiCharts. If any modification or cancel command is generated by the code in MultiCharts – it is sent to the broker.

Usually such commands are generated and processed in MultiCharts within milliseconds.

From MultiCharts logs we can measure the time from generating the command and sending it outside of MultiCharts (broker API), and the time from receiving the reply command outside of MultiCharts (broker API) until processing it and displaying the status in MultiCharts interface. MultiCharts cannot affect the possible Internet latency and/or the broker order processing speed, as well as the broker sending the order status.

Order and Position tracker shows local PC time. Some millisecond delay is possible between MultiCharts receiving the order status and processing it, showing it on the OPT window.

Wilkinsw, as for the your particular case, as we have already discussed in the email correspondence, please send me the MultiCharts logs and OPT tabs export so that we can study them and provide the analysis: how long did it take to generate the order in MultiCharts, process it and send the order command to the broker, when did the broker provide the order status reply.

I will ask our developers if that is possible to create a code for measuring the code calculation speed.

Re: Latency / slow order submission. Please share experience

Thanks for the reply Henry. It's made a few things clearer.

So what might look like latency is in fact a whole raft of confirmations going back and forth which make it appear to delay the order submission speed but, from what you say, it is probably taking milliseconds on Multicharts' end to calculate and submit.

I haven't sent you logs re the Sunday night missed fill because, as mentioned previously, logging was off due to another issue I've been struggling with.

However there is definitely a lag somewhere otherwise I would have got that fill on Sunday night (>1second window). My colleague (as you know he also uses MC) also missed the fill.

Therefore, now I have logging back on, I will send you my logs for analysis to see if there are any obvious signs of latency since I last restarted MC (yesterday evening).

I still need to carry out the ping tests that MAtricks kindly advised me to do.

Some way of calculating code calc speed will be great and I'd imagine would be a useful tool to many system developers using MC.

Thanks!

So what might look like latency is in fact a whole raft of confirmations going back and forth which make it appear to delay the order submission speed but, from what you say, it is probably taking milliseconds on Multicharts' end to calculate and submit.

I haven't sent you logs re the Sunday night missed fill because, as mentioned previously, logging was off due to another issue I've been struggling with.

However there is definitely a lag somewhere otherwise I would have got that fill on Sunday night (>1second window). My colleague (as you know he also uses MC) also missed the fill.

Therefore, now I have logging back on, I will send you my logs for analysis to see if there are any obvious signs of latency since I last restarted MC (yesterday evening).

I still need to carry out the ping tests that MAtricks kindly advised me to do.

Some way of calculating code calc speed will be great and I'd imagine would be a useful tool to many system developers using MC.

Thanks!

Re: Latency / slow order submission. Please share experience

I agree about it being slow... I upgraded my computer because I thought that was the problem and now have a pretty nice machine (8 core AMD, 16 gig RAM, SSD hard drives) and still see some latency. I tried SC (non .net version) and it executes my orders substantially faster. Sometimes by the time my order shows up price has moved 2-3 ticks

Re: Latency / slow order submission. Please share experience

gpw797, thanks for sharing.

Henry, if you could just confirm (or correct me) that the reason gpw797 might see a lag in their order showing up is due to the confirmation process needing to take place first between MC and the broker before that order shows up.

But, critically, the order has already been submitted to the broker before the order shows up on his ront end.

I hope I got it right.

Henry, if you could just confirm (or correct me) that the reason gpw797 might see a lag in their order showing up is due to the confirmation process needing to take place first between MC and the broker before that order shows up.

But, critically, the order has already been submitted to the broker before the order shows up on his ront end.

I hope I got it right.

Re: Latency / slow order submission. Please share experience

Another thing to consider would be the order type and where price was as the order was being placed. If two people received the same nonfill with the same strategy, I would look at the how the execution is coded.

Re: Latency / slow order submission. Please share experience

I don't know the exact details of my colleague's strategy.

My strategy literally submitted a buy limit order for CL at 103.05. Submitted following the calculation of my code after the first tick after 1800 est / 2300 gmt on 02/03/2014.

The time between the first tick and the offer exceeding 103.05 was 1.015 seconds. So don't understand why I wasn't filled.

My strategy literally submitted a buy limit order for CL at 103.05. Submitted following the calculation of my code after the first tick after 1800 est / 2300 gmt on 02/03/2014.

The time between the first tick and the offer exceeding 103.05 was 1.015 seconds. So don't understand why I wasn't filled.

-

JoshM

- Posts: 2195

- Joined: 20 May 2011

- Location: The Netherlands

- Has thanked: 1544 times

- Been thanked: 1565 times

- Contact:

Re: Latency / slow order submission. Please share experience

I thought like this, but feedback is welcomed since it seems a little quick to me:What might be the equivalent in Multicharts (down to milliseconds)? Is there a stopwatch / milliseconds DLL timer type thing I can use?

Code: Select all

Variables:

dtBegin(0), dtEnd(0), oneMS(1/86400000);

if (BarStatus(1) = 2) then begin

dtBegin = ComputerDateTime;

for value20 = 0 to 100 begin

for value1 = 0 to 100 begin

value2 = Average(Close[value1], 20);

value3 = Average(High[value1], 20);

value4 = Average(Low[value1], 20);

value5 = Average(Open[value1], 20);

end; //: Inner loop

end; //: Outmost loop

dtEnd = ComputerDateTime;

Print("Execution time (ms): ",

(dtEnd - dtBegin) / oneMS);

end; // OnBarClose

Code: Select all

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 62.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 79.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 62.00

Execution time (ms): 94.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 62.00

Execution time (ms): 78.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 62.00

Execution time (ms): 63.00

Execution time (ms): 78.00

Execution time (ms): 63.00

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency. Please share experiences.

Please find our sample code attached.

- Attachments

-

- calculate_time_ms.pla

- (2.96 KiB) Downloaded 649 times

Re: Latency. Please share experiences.

Hi,

Thanks for that. I know I must be doing something wrong:

When I add your indicator using the ADX example in the code......It takes a while to load (that'll be the loop) but then all I get in the output is:

"execTime = 0.00000"

What have I done wrong?

Thanks for that. I know I must be doing something wrong:

When I add your indicator using the ADX example in the code......It takes a while to load (that'll be the loop) but then all I get in the output is:

"execTime = 0.00000"

What have I done wrong?

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency. Please share experiences.

"execTime = 0.00000" means the code was calculated very fast, there is nothing wrong with it.

Re: Latency / slow order submission. Please share experience

Right. For those following this thread, I still haven't found a comprehensive answer as to why it took >1sec to recognise the opening first trade of the session and get my order to market.1 full second is extremely bad latency. MC should process your orders within a few microseconds on your side of things. Although its the easiest to blame, I doubt its your machine. Your connection is almost always the issue.

1. Download PingPlotter to your trading machine

2. Find the relevant IPs for IQ and Pats

3. Do a round trip ping test to IQ feeds servers (my average is 2ms)

4. Do a round trip ping test to Pats Order servers (my average is 2ms)

5. Add that up and double it for good measure

I'd love to hear from the MC team on this as well. I'm curious how "fast" this software is.

However I've found some answers and have made some progress re solutions.

Firstly:

Ping tests: IQfeed servers (from London) =140ms London Patsystems servers = 3ms Totalx2 (see MAtricks) = 286ms ......a whopping 1/3 of a second.

Secondly:

Multicharts script calculation speed: Not an issue ..... a few microseconds (forget milli!).

Thirdly:

API plugin / API limitations. Please contact Henry for more information regarding this. In a nutshell when multiple orders are submitted to the same API account, in an instance (such as market open) they are queued and submitted one at a time. This can be improved by having multiple API accounts (and multiple cores using each account). I haven't been able to nail down a specific delay to this particular bottle neck.

Fourthly:

Computer limitations. I think my computer may have not been able to efficiently handle the acute load with 17 charts all submitting orders at virtually the same exact millisecond event (the open).

Conclusion and Solutions:

Firstly. Most of the third of a second datefeed/trade server latency can be saved with a better selected remote server location. If you can get colocated then even better. For example, if I switched to the much more expensive TT API that Marex offer then I'll be colocated at the Cermak datacentre in Chicago. However, I think I'll be looking at about £1000pm for that vs. Pats's £40pm (not inc Jtrader). Can't afford this at the moment. Unfortunately my nearest Pats trade server to Chicago is London.

Secondly. I have just upgraded to a server with 8GB Ram and an Intel Xeon E5-2620v2 2.10Ghz processor.

Thirdly. To help avoid API plugin bottlenecks.

1) Use GTC/D orders. Most ideally exchange supported GTCs. Your orders are then already part of the premarket order book building process, bypassing the acutely demanding event of the open on Multicharts and your computer. If not exhange supported GTCs and are instead synthetic then: Your broker will be responsible for getting your orders to market AT the open. Question is; who is faster. You and your computer or the broker? Do you trust your broker? etc etc.

Finally, to help avoid event driven overload, that also occurs when multiple bars on different charts all close at the same interval*, it might be worth considering having bars close on unusual minutes. E.g. GC=59past...HG=58past....EU=57 past etc etc instead of 00 on the hour when using 60min timeframe. Or alternatively acheive the same effect but with IOG=ON and creating the calculation event on an unconventional interval.

I hope my findings help. Basically, ping tests, computer power, bottleneck workarounds and emails to your broker!

*but note that the variance in milliseconds of when the first tick of the new bar arrives for all your instruments is far larger and hence less of an issue than the first tick that arrives at the start of a new session (which for my CME group products will all arrive well within the same millisecond!). Hence the open is still, by far, a more demanding issue and the bigger driver of latency.

Last edited by wilkinsw on 27 Mar 2014, edited 2 times in total.

Re: Latency. Please share experiences.

Good to hear that you are nailing down the issue. 1/3 of a second is hideous  and most definitely a lot of the issue.

and most definitely a lot of the issue.

If you can lower that latency, that'd be great. If not, I'd suggest looking into switching things to AA mode. This will cut your latency issues in half seeing as MC will not have to confirm orders on its end.

I'm a little unsure of the process of exact process of things. I think this is how it works-

SA mode: 1. Data to MC, 2. MC to Order Server, 3. Order Server to MC.

AA mode: 1. Data to MC 2. MC to Order Server.

Henry or Andrew, could you confirm?

If you can lower that latency, that'd be great. If not, I'd suggest looking into switching things to AA mode. This will cut your latency issues in half seeing as MC will not have to confirm orders on its end.

I'm a little unsure of the process of exact process of things. I think this is how it works-

SA mode: 1. Data to MC, 2. MC to Order Server, 3. Order Server to MC.

AA mode: 1. Data to MC 2. MC to Order Server.

Henry or Andrew, could you confirm?

-

JoshM

- Posts: 2195

- Joined: 20 May 2011

- Location: The Netherlands

- Has thanked: 1544 times

- Been thanked: 1565 times

- Contact:

Re: Latency / slow order submission. Please share experience

I would not put a terrible amount of faith in ping numbers. For example:Ping tests: IQfeed servers (from London) =140ms London Patsystems servers = 3ms Totalx2 (see MAtricks) = 286ms ......a whopping 1/3 of a second.

From Paris to Tokyo: On the Suitability of ping to Measure Latency (pdf)Monitoring Internet performance and measuring user quality of experience are drawing increased attention from both research and industry. To match this interest, large-scale measurement infrastructures have been constructed. We believe that this effort must be combined with a critical review and calibrarion of the tools being used to measure performance.

In this paper, we analyze the suitability of ping for delay measurement. By performing several experiments on different source and destination pairs, we found cases in which ping gave very poor estimates of delay and jitter as they might be experienced by an application. In those cases, delay was heavily dependent on the flow identifier, even if only one IP path was used. For accurate delay measurement we propose to replace the ping tool with an adaptation of paris-traceroute which supports delay and jitter estimation, without being biased by per-flow network load balancing.

Also interesting: Don’t use ping for accurate delay measurements.

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency. Please share experiences.

That is not corect. The speed and procedure of communication with the broker is the same when using SA and AA mode.If not, I'd suggest looking into switching things to AA mode. This will cut your latency issues in half seeing as MC will not have to confirm orders on its end.

I'm a little unsure of the process of exact process of things. I think this is how it works-

SA mode: 1. Data to MC, 2. MC to Order Server, 3. Order Server to MC.

AA mode: 1. Data to MC 2. MC to Order Server.

Henry or Andrew, could you confirm?

Re: Latency. Please share experiences.

Thanks Henry.

So MC does confirm a fill on the orders in AA mode? It sure doesn't seem like it.. but I stand corrected.

I'd really like to understand the paths that MC takes. Is there a flow chart or a quick description of them somewhere?

So MC does confirm a fill on the orders in AA mode? It sure doesn't seem like it.. but I stand corrected.

I'd really like to understand the paths that MC takes. Is there a flow chart or a quick description of them somewhere?

Re: Latency. Please share experiences.

I second that. Would absolutely love a schematic or just a better description of the communications that take place.Thanks Henry.

So MC does confirm a fill on the orders in AA mode? It sure doesn't seem like it.. but I stand corrected.

I'd really like to understand the paths that MC takes. Is there a flow chart or a quick description of them somewhere?

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency. Please share experiences.

You can share the log analysis I have sent you on 3/6/2014. It contains detailed description of each event that took place.I second that. Would absolutely love a schematic or just a better description of the communications that take place.

Re: Latency. Please share experiences.

As requested:

Hello William,

Our engineers have studied the logs from your PC for the orders in question.

Here are the details of order generation and API replies with the time stamps with millisecond precision.

All timestamps are Local time = correspond to your computer clock.

PATS API replies (as far as we know they mean the following):

Queued - Order accepted by the API (API dll on your local PC)

Sent - Order sent to the server

Working - Order accepted by the exchange

Order #6012496

23:00:00.709 (inside MultiCharts) - order is generated and sent to the trading plugin

23:00:00.726 (MultiCharts to API): command to send the order to the API. Place Order (Buy stop-limit order Quantity = 1, StopPrice = 1354.700000, LimitPrice = 1355.500000)

23:00:00.738 (from API to MultiCharts): Queued

23:00:00.747 (from API): Sent

23:00:01.206 (from API): Working

No further status updates for this order in the logs.

Order #6012498

23:00:01.495 (MC) - order is generated and sent to the trading plugin

23:00:01.507 (to API): Place Order (Buy stop order Lots: 1 ; Stop Price: 1340.9)

23:00:01.511 (from API): Queued

23:00:01.520 (from API): Sent

23:00:02.004 (from API): Working (Lots: 1 ; Stop Price: 1340.9)

08:45:12.752 (to API): Order modify

08:45:12.783 (from API): AmendPending (Lots: 1 ; Stop Price: 1339.3)

08:45:13.080 (from API): Working (Lots: 1 ; Stop Price: 1339.3)

09:15:03.297 (to API): Order modify

09:15:03.328 (from API): AmendPending (Lots: 1 ; Stop Price: 1338.3)

09:15:03.593 (from API): Working (Lots: 1 ; Stop Price: 1338.3)

Order has become a Limit order (no commands from MultiCharts to change the order type, possibly order type changed by broker or via broker platform) and got executed at once.

13:16:07.403 (from API): Working (Lots: 1 ; Limit Price: 1343.3)

13:16:07.403 (from API): Filled (Lots: 1 ; Limit Price: 1343.3 ; FillPrice: 1338.4)

Order #6012499

23:00:01.495 (MC) - order is generated and sent to the trading plugin

23:00:01.510 (to API): Place Order (Buy Limit order Lots: 1 ; Price: 1310.4)

23:00:01.515 (from API): Queued

23:00:01.525 (from API): Sent

23:00:02.012 (from API): Working

13:16:07.497 (to API): Cancel order

13:16:07.497 (from API): CancelPending

13:16:07.778 (from API): Cancelled

As you can see it takes milliseconds to get the order generated in MultiCharts and sent to the broker API.

Then it takes about half a second for the broker API to get the order active at broker/exchange.

After the order is active at broker/exchange – the broker is in charge of order execution price and time.

Re: Latency. Please share experiences.

A schematic of some kind would still be of value, at least to me.

order #6012496 and order #6012498 in the above logs were for the same instrument and generated from two different charts. So why 0.7 seconds difference in sending the order to the plugin? Both had the same event trigger their calculations (first tick of the open) and both were identical strategies (bar small differences in a few variables).

Is this the API plugin order queuing that you described to me before?

order #6012496 and order #6012498 in the above logs were for the same instrument and generated from two different charts. So why 0.7 seconds difference in sending the order to the plugin? Both had the same event trigger their calculations (first tick of the open) and both were identical strategies (bar small differences in a few variables).

Is this the API plugin order queuing that you described to me before?

Re: Latency. Please share experiences.

Interesting point, that I missed.Why does it only take micro seconds to generate and send the command to cancel the order but it takes several milliseconds to generate an order?

Re: Latency. Please share experiences.

I had been running a Mac (fairly new model) with VMWare to run MC. My machine slowed with time and I had one WS open with 3 data series, that's it. A few months ago I purchased a PC (old school, CPU on the floor) with 12 GB RAM and a pretty fast processor. To say the PC is faster is an understatement. Night and day. If you are serious about your trading and the time you likely spending developing on MC then invest in a dedicated and fast machine.

Re: Latency. Please share experiences.

Agreed! MC does require a boat load of performance to run smoothly for the heavy user. As I've noticed since moving onto a server in our office.If you are serious about your trading and the time you likely spending developing on MC then invest in a dedicated and fast machine.

The company I work for spent £6000 on this brand new monster of a server. The IT guy has gradually ramped up my allocation of cores and the handling of MC significantly changed with each core added. Having said that I still am having some issues with the Pats plugin (but I think that's another story).

My setup now:

Intel Xeon CPU E5-2620 v2 2.1Ghz.... 8 cores on my VM.

8GB Ram

Windows Server 2012 R2.

Re: Latency. Please share experiences.

I have not used Pats, only IB in testing (and will never touch them for anything in the future). My client is using TT and I must say that it is working beautifully. Getting off subject but after spending nearly nine months in development and then going "live" three surprises popped out at me that you never see in development, (1) clock syncing, (2) broker connection and (3) data providers. If you are testing and in development, I strongly suggest you do (1) daily (either manually or edit the registry to do daily, currently weekly), (2) and (3) research now before going live whether your own trading or for a client.

I run IQ at my home and my client runs TT. Clocks are synced daily for each of us and yet the results still vary at times. Sometimes pretty significantly. If I had known this prior, I would have pushed the client to run IQ and not TT. There are a lot of components to MC beyond the machine. I never realized just how much in development.

I run IQ at my home and my client runs TT. Clocks are synced daily for each of us and yet the results still vary at times. Sometimes pretty significantly. If I had known this prior, I would have pushed the client to run IQ and not TT. There are a lot of components to MC beyond the machine. I never realized just how much in development.

Re: Latency. Please share experiences.

Will look at this.Clocks are synced daily

That's good to know. Thanks.My client is using TT and I must say that it is working beautifully.

What results vary?Clocks are synced daily for each of us and yet the results still vary at times. Sometimes pretty significantly.

Would love some more info around this from you, Henry or anyone who cares to share. I've still got very significant latency beyond the hop across the Atlantic from London. Want to know precisely why. Not with the aim of slinging mud or trying to show anyone up, just so I know what I'm dealing with. For the record I think MC is a great value for money product.There are a lot of components to MC beyond the machine.

Re: Latency. Please share experiences.

I'll finish my two cents by saying I love MC as a product (and their support group). They have done and continue to do a fantastic job. Many of these elements I speak of are in a way beyond their control. Data providers for example. There are how many exchanges these days? Lot of data that needs to be fed to our machine and who you pick can vary by speed and filtering. I tip my hat to the MC crew. I've been running the software for about a year now and it is very stable. And they work with so many data providers, brokers, etc. Glad I chose them versus NT or TS for example. Including being able to send a file in .sef format and not be concerned about my code be decompiled. They really thought pretty much everything through. Now I'm way off topic and will stop yapping.

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency. Please share experiences.

Please specify the particular lines you are referring to.Why does it only take micro seconds to generate and send the command to cancel the order but it takes several milliseconds to generate an order?

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency. Please share experiences.

That is correct.A schematic of some kind would still be of value, at least to me.

order #6012496 and order #6012498 in the above logs were for the same instrument and generated from two different charts. So why 0.7 seconds difference in sending the order to the plugin? Both had the same event trigger their calculations (first tick of the open) and both were identical strategies (bar small differences in a few variables).

Is this the API plugin order queuing that you described to me before?

One trading plugin can process 1 order per time. It means all orders that are generated by the strategy are put into a queue and sent one by one to the API. Once one order is sent, the trading engine starts sending the next order. That is not technically possible to send two orders simultaneously to one API.

If there are two APIs (two different brokers) – then two orders can be sent almost at the same time.

In order to perform such high speed calculations you need a CPU with 4 cores or more.

Each chart with a strategy will get one flow.

Each trading instance will get one flow.

4 cores can get 1 flow each and supply parallel calculation.

But if you have a single broker profile then the amount of cores you have will not help to process the orders faster.

Re: Latency. Please share experiences.

I don't fully understand what MAtricks is referring to (I don't see the difference to the extent he's stating) but it is still interesting that there is a difference of a few milliseconds:Please specify the particular lines you are referring to.MAtricks wrote:

Why does it only take micro seconds to generate and send the command to cancel the order but it takes several milliseconds to generate an order?

To send cancel and confirm cancelled = 13:16:07.778 - 13:16:07.497 = 281 millisecondsOrder #6012499

23:00:01.495 (MC) - order is generated and sent to the trading plugin

23:00:01.510 (to API): Place Order (Buy Limit order Lots: 1 ; Price: 1310.4)

23:00:01.515 (from API): Queued

23:00:01.525 (from API): Sent

23:00:02.012 (from API): Working

13:16:07.497 (to API): Cancel order

13:16:07.497 (from API): CancelPending

13:16:07.778 (from API): Cancelled

To place order and confirm working = 23:00:02.012 - 23:00:01.510 = 502 milliseconds....twice as long

To send modify and confirm modified is also about 300 milliseconds.

Therefore, correct me if I'm wrong:

As the place orders were all sent at the open and as they took significantly longer than the modify/cancel orders (which took place at varying times of non significance)....one can isolate that submitting orders at demanding times will cost me (using Patsystems) an extra 2/10s of a second. Just because of the extra load on Patsystems at this time.

Wow that's poor latency from Pats (unless I've missed something)! Even low load times when instruction were submitted still take 2/10s of a second anyway just because of that annoying distance between the UK and the US!

But what is particularly scary is that the Pats broker plugin queue costed me (in the logs above) approx 7/10s of a second!! In the case study where I missed the CL fill I had almost all my charts and instruments firing orders at the opening tick. Therefore I think the plugin queue cost me far more than 7/10 of a second as in the lower load open in the logs above. Again, the high load of the open on my PC probably exacerbated this. What I need to do is see what this figure is like for when two modify/cancel orders are submitted at the same time intraday.

Ok, so I feel like I'm much closer to fully understanding where latency lies.

Imagining I'm colocated: Latency, using one PATS API account is:

high load (session opening tick): Patsystems API: approx 0.3 seconds.....MC: approx 0.7+ seconds (virtually all of which is from the broker plugin queue). = approx 0.9+ seconds!

low load: Patsystems API: approx 0.1 seconds or less......MC: approx a few millionths of a seconds AS LONG AS no simultaneous orders are sent..in which case can be up to 0.7 seconds.

=0.1 seconds or less

Conclusions: See previous conclusions (GTC/D orders, computer power, server location etc), but also:

Use multiple broker accounts. If my assessment is correct and the high load example cost an extra 0.2 seconds just from the Pats API then maybe look at other brokers (but Pats is very cheap)?

Last edited by wilkinsw on 10 Apr 2014, edited 2 times in total.

Re: Latency. Please share experiences.

Code: Select all

13:16:07.497 (to API): Cancel order

13:16:07.497 (from API): CancelPending

This cancel order is unique to that according to the few examples given.

Location is everything.

Re: Latency. Please share experiences.

Can I use two different Pats API accounts? Or does it have to be two different API target servers too?That is not technically possible to send two orders simultaneously to one API.

If there are two APIs (two different brokers) – then two orders can be sent almost at the same time.

In order to perform such high speed calculations you need a CPU with 4 cores or more.

Each chart with a strategy will get one flow.

Each trading instance will get one flow.

4 cores can get 1 flow each and supply parallel calculation.

But if you have a single broker profile then the amount of cores you have will not help to process the orders faster.

-

Henry MultiСharts

- Posts: 9165

- Joined: 25 Aug 2011

- Has thanked: 1264 times

- Been thanked: 2958 times

Re: Latency. Please share experiences.

You need to have two PATS logins/two separate PATS broker profiles - this should bring up two API instances.Can I use two different Pats API accounts? Or does it have to be two different API target servers too?That is not technically possible to send two orders simultaneously to one API.

If there are two APIs (two different brokers) – then two orders can be sent almost at the same time.

In order to perform such high speed calculations you need a CPU with 4 cores or more.

Each chart with a strategy will get one flow.

Each trading instance will get one flow.

4 cores can get 1 flow each and supply parallel calculation.

But if you have a single broker profile then the amount of cores you have will not help to process the orders faster.

Re: Latency. Please share experiences.

Ok great. I'll test this solution with another Pats account soon. Based on the findings above it should have a massive effect on reducing latency. If I you use one broker account profile (Api instance) per core I'll be getting close to halving the latency I currently experience.

This is something that anyone trading from a large number of charts should consider IMHO.

This is something that anyone trading from a large number of charts should consider IMHO.

-

PatrickSocal

- Posts: 58

- Joined: 27 Apr 2013

- Location: San Diego, CA

- Has thanked: 23 times

- Been thanked: 30 times

Re: Latency. Please share experiences.

Hi Wil,Hi,

Thanks for that. I know I must be doing something wrong:

When I add your indicator using the ADX example in the code......It takes a while to load (that'll be the loop) but then all I get in the output is:

"execTime = 0.00000"

What have I done wrong?

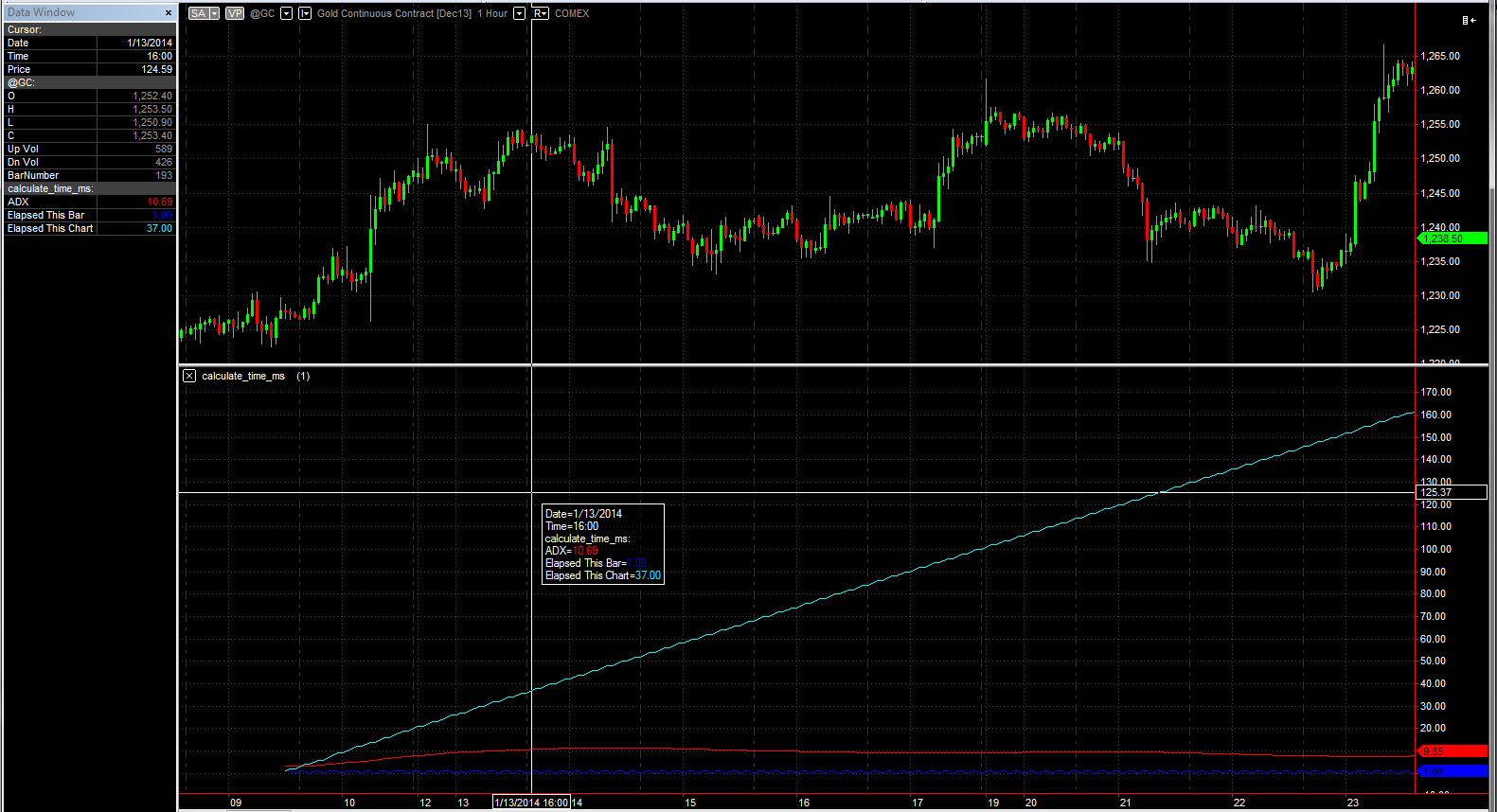

I just checked that calculate_ms indicator, and it does work, but I modified it a bit to be more instructive. Here's a screenshot:

The system call they've used has a resolution of about 15-16 ms. So it increments gradually over the chart, as you can see in the cyan line. I'm attaching the code for this modified version.

Hope that helps...

- Attachments

-

- calculate_time_ms_2.pla

- (1.46 KiB) Downloaded 459 times

-

- calculate_time_ms.png

- (76.01 KiB) Downloaded 7460 times

-

PatrickSocal

- Posts: 58

- Joined: 27 Apr 2013

- Location: San Diego, CA

- Has thanked: 23 times

- Been thanked: 30 times

Re: Latency. Please share experiences.

Hi again... Just for fun, I also did a test using the "computerdatetime" function. It has much finer resolution on my machine (around 1 ms), compared to the "calculate_time_ms" function (around 15 ms). Compare the following chart to the one in my last post:

I'm including the code for the modified indicator as calculate_time_ms_3.pla

You can change the input argument from 1 to 2 to see how the different timers perform on your machine. Happy times...

I'm including the code for the modified indicator as calculate_time_ms_3.pla

You can change the input argument from 1 to 2 to see how the different timers perform on your machine. Happy times...

- Attachments

-

- computerdatetime_vs_calculate_time_ms.png

- (75.95 KiB) Downloaded 7504 times

-

- calculate_time_ms_3.pla

- (4.45 KiB) Downloaded 454 times

Re: Latency. Please share experiences.

Agree, its a little confusing.Hi,

Thanks for that. I know I must be doing something wrong:

When I add your indicator using the ADX example in the code......It takes a while to load (that'll be the loop) but then all I get in the output is:

"execTime = 0.00000"

What have I done wrong?

It gives the result as 0.00000 for calculation over a single bar. Resolution of timer is around 15 ms, so it will show 0.00000 if time taken to calculate ADX (or any other indicator or your strategy) on one bar is < 15ms. This will be true for almost all the cases.

What you should do to get a useful value is to modify the first line as follows:

Code: Select all

if barnumber = 1 then value1 = calculate_ms;Re: Latency. Please share experiences.

Hello PatrickSocial, I think you should modify your code as follows:Hi again... Just for fun, I also did a test using the "computerdatetime" function. It has much finer resolution on my machine (around 1 ms), compared to the "calculate_time_ms" function (around 15 ms).

Code: Select all

//start_ms = MillisecondsFromDateTime(computerdatetime)

start_ms = MillisecondsFromDateTime(computerdatetime)+secondsFromDateTime(computerdatetime)*1000Code: Select all

//value2 = MillisecondsFromDateTime(computerdatetime)

value2 = MillisecondsFromDateTime(computerdatetime)+secondsFromDateTime(computerdatetime)*1000I am not sure what underlying windows call has MC used while implementing computerdatetime.

-

PatrickSocal

- Posts: 58

- Joined: 27 Apr 2013

- Location: San Diego, CA

- Has thanked: 23 times

- Been thanked: 30 times

Re: Latency. Please share experiences.

Hi Hilbert,

Yes, if you want to handle rollover effects, the code should be modified to handle seconds, minutes, hours, days, etc. I was just keeping it simple. Code that handles second, minute and hour rollovers (but not days or longer) would look like this:

So if you start your test at 3:59:59 and it takes more than a second, it should work. But if you start it at 23:59:59 it won't. And if the test takes more than one day, it also won't... But your computer is probably faster than that

Actually, a better way to do it is to calculate the differences in terms of DateTime, and then compute the milliseconds from that difference. That way, you handle all rollover effects, and you can measure multi-day time differences too (in the unlikely event that you need to). My modified code looks like this:

Regarding the more tricky question of irregular resolution behavior... I haven't seen it on my machines. As you see in the above code, I computed a max-value on the time elapsed per bar. I tried it on a chart with about 65,000 bars, and it was never more than 3 ms on my machine. Average time per bar was about 0.6 ms. This was using a Lenovo W530 with a 4-core i7-3820QM processor with hyperthreading turned off, running Win7. In fact, I just tried again on a chart with 350k bars, and again, the resolution was consistent. Now it got a max of 5 ms, but still an average of 0.6 ms. Here's a screenshot:

What kind of hardware are you using to get your results? If you have access to another machine, perhaps it would be worth trying it there? Also, I'm attaching my indicator in case you want to try it.

Hope this helps...

Yes, if you want to handle rollover effects, the code should be modified to handle seconds, minutes, hours, days, etc. I was just keeping it simple. Code that handles second, minute and hour rollovers (but not days or longer) would look like this:

Code: Select all

start_ms = MillisecondsFromDateTime(computerdatetime) + 1000*SecondsFromDateTime(computerdatetime) + 60000*MinutesFromDateTime(computerdatetime) + 3600000*HoursFromDateTime(computerdatetime)Actually, a better way to do it is to calculate the differences in terms of DateTime, and then compute the milliseconds from that difference. That way, you handle all rollover effects, and you can measure multi-day time differences too (in the unlikely event that you need to). My modified code looks like this:

Code: Select all

Variables:

ii(0),

start_DateTime(0), end_DateTime(0),

deltaDateTimeBar(0), deltaDateTimeChart(0),

elapsedThisBar(0), elapsedThisChart(0),

maxElapsedPerBar(0), myCount(0), mySum(0);

Once start_DateTime = computerdatetime;

For ii=0 To 10000 Begin // Do something slow

value3=ADX(140);

End;

end_DateTime = computerdatetime;

if end_DateTime[1] > 0 then begin

deltaDateTimeBar = end_DateTime - end_DateTime[1];

deltaDateTimeChart = end_DateTime - start_DateTime;

elapsedThisBar = MillisecondsFromDateTime(deltaDateTimeBar) +

1000*SecondsFromDateTime(deltaDateTimeBar) +

60000*MinutesFromDateTime(deltaDateTimeBar) +

3600000*HoursFromDateTime(deltaDateTimeBar) +

86400000*floor(deltaDateTimeBar);

elapsedThisChart = MillisecondsFromDateTime(deltaDateTimeChart) +

1000*SecondsFromDateTime(deltaDateTimeChart) +

60000*MinutesFromDateTime(deltaDateTimeChart) +

3600000*HoursFromDateTime(deltaDateTimeChart) +

86400000*floor(deltaDateTimeChart);

maxElapsedPerBar = maxlist(maxElapsedPerBar, elapsedThisBar);

myCount += 1;

mySum += elapsedThisBar;

plot1( value3, "ADX");

Plot2(elapsedThisBar, "Elapsed This Bar");

Plot3(elapsedThisChart, "Elapsed This Chart");

Plot4(maxElapsedPerBar, "Max Elapsed Per Bar");

Plot5(mySum / myCount, "Average Elapsed Per Bar");

end;

What kind of hardware are you using to get your results? If you have access to another machine, perhaps it would be worth trying it there? Also, I'm attaching my indicator in case you want to try it.

Hope this helps...

- Attachments

-

- calculate_time_ms_4.pla

- (6.41 KiB) Downloaded 440 times

-

- calculate_time_ms_4.png

- (44.67 KiB) Downloaded 7359 times

-

virginiatrader

- Posts: 79

- Joined: 05 May 2007

- Location: Virginia

- Has thanked: 5 times

- Been thanked: 5 times

Re: Latency. Please share experiences.

wilkinsw, and to all who have left comments and guidance...

I read the entire string from beginning to end, and I am always thankful that I am an MC user and member of the forum. I never fail to learn something new each time I am here.

While I have traded in real-time off MC 15 minute charts of the E-Mini S&P500, I didn't do it with MC as an automated platform. I am primarily an end-of-day futures trader, using MC to chart and analyze my markets, and have coded very simple trend-following systems using PowerLanguage.

I monitor my markets and charts daily, and should I miss entering or exiting a trade, or should MC fail to "fire" a signal when I expect it to (yes, it has happened), my trading plan allows me to enter or exit on a discretionary basis, so while I may be late to the trade, i do not miss it entirely.

wilkinsw, and everyone, I am curious: if you miss your fill, why not enter the order manually? While "going retail" with a market order is not always preferable, it does get you into the trade. Or, as an alternative, use a "marketable limit" order, i.e., hit the bid or lift the offer and then follow the trade according to your template.

Just wondering...

virginiatrader

I read the entire string from beginning to end, and I am always thankful that I am an MC user and member of the forum. I never fail to learn something new each time I am here.

While I have traded in real-time off MC 15 minute charts of the E-Mini S&P500, I didn't do it with MC as an automated platform. I am primarily an end-of-day futures trader, using MC to chart and analyze my markets, and have coded very simple trend-following systems using PowerLanguage.

I monitor my markets and charts daily, and should I miss entering or exiting a trade, or should MC fail to "fire" a signal when I expect it to (yes, it has happened), my trading plan allows me to enter or exit on a discretionary basis, so while I may be late to the trade, i do not miss it entirely.

wilkinsw, and everyone, I am curious: if you miss your fill, why not enter the order manually? While "going retail" with a market order is not always preferable, it does get you into the trade. Or, as an alternative, use a "marketable limit" order, i.e., hit the bid or lift the offer and then follow the trade according to your template.

Just wondering...

virginiatrader

Re: Latency. Please share experiences.

I don't know if this is the 'main' cause of the lag being reported but you should be aware that a 1-tick lag exists, by design, when submitting 'Next Bar' orders with IOG-ON. The resultant lag is difficult to spot during RTH as there are so many ticks but the potential for adverse consequences exists regardless of time-of-day.

e.g.

The following example assumes a downward moving market and the placing of a trailing Buy Stop. An order has already been sent to Buy Next Bar @ 100 on a Stop and is visible on the book.

So, a Buy Stop is @ 100

Tick 1 - Market moves down a tick so an order is generated in the MC script to move the Stop to 99.

However, the order at the broker remains @ 100 even though the script requested it to be moved to 99.

Tick 2 - The order at the broker changes to 99 - Correct but one tick after the order was first generated.

Tick 3 - Market moves down again so an order is generated in the MC script to move the Stop to 98 ...

The order at the broker remains @ 99 even though the script requested it to be moved to 98.

Tick 4 - The order at the broker changes to 98 - Correct but one tick after the order was first generated.

etc. etc.

Any delays risk fills being missed but it also runs the risk of orders being filled when they shouldn't be. Both can result in significant losses either due to missing a good move or being stopped out too early while in a move.

Of course, there is always going to be some lag between issuing an order and that order reaching the exchange but this is a case where it is MC itself that is adding to that lag by also sending these orders one tick after the fact. I consider this to be a bug/flaw – not in the code (that’s doing what it was designed to do) but in the design itself. I can't think of a single reason why such a design would be anything but a liability and I see no potential benefit. Other ATM platforms don't have this lag (so it's avoidable) and I can't think any reason why someone would introduce it into their design if say, they were writing directly to the broker's API. If I've missed a really good reason, I'd love to hear it.

I think it's great that MC is continually seeking ways to improve performance but it seems strange to continue with a design that is deliberately (and unnecessarily IMO) inserting lag.

e.g.

The following example assumes a downward moving market and the placing of a trailing Buy Stop. An order has already been sent to Buy Next Bar @ 100 on a Stop and is visible on the book.

So, a Buy Stop is @ 100

Tick 1 - Market moves down a tick so an order is generated in the MC script to move the Stop to 99.

However, the order at the broker remains @ 100 even though the script requested it to be moved to 99.

Tick 2 - The order at the broker changes to 99 - Correct but one tick after the order was first generated.

Tick 3 - Market moves down again so an order is generated in the MC script to move the Stop to 98 ...

The order at the broker remains @ 99 even though the script requested it to be moved to 98.

Tick 4 - The order at the broker changes to 98 - Correct but one tick after the order was first generated.

etc. etc.

Any delays risk fills being missed but it also runs the risk of orders being filled when they shouldn't be. Both can result in significant losses either due to missing a good move or being stopped out too early while in a move.

Of course, there is always going to be some lag between issuing an order and that order reaching the exchange but this is a case where it is MC itself that is adding to that lag by also sending these orders one tick after the fact. I consider this to be a bug/flaw – not in the code (that’s doing what it was designed to do) but in the design itself. I can't think of a single reason why such a design would be anything but a liability and I see no potential benefit. Other ATM platforms don't have this lag (so it's avoidable) and I can't think any reason why someone would introduce it into their design if say, they were writing directly to the broker's API. If I've missed a really good reason, I'd love to hear it.

I think it's great that MC is continually seeking ways to improve performance but it seems strange to continue with a design that is deliberately (and unnecessarily IMO) inserting lag.

Re: Latency. Please share experiences.

I've written a java program that places an order with IB via TWS-API.

I've used the same logic in an MC-indicator and compared the execution times

Multicharts was always approx. 100ms slower to place the same order than my java program. C++ would probably be even faster

I've used the same logic in an MC-indicator and compared the execution times

Multicharts was always approx. 100ms slower to place the same order than my java program. C++ would probably be even faster

Re: Latency. Please share experiences.

gerler, can you give some more color on what was measured. Specifically, the time being 100ms longer: what events bracket the time interval in both the MC code and your Java code?

Re: Latency. Please share experiences.

Hi Gerler that is pretty amazing time saving - any chance you can share your methodology with either MC so they could develop into next release or alternatively could you offer some configurable add on for broker API's too?I've written a java program that places an order with IB via TWS-API.

I've used the same logic in an MC-indicator and compared the execution times

Multicharts was always approx. 100ms slower to place the same order than my java program. C++ would probably be even faster

Thanks.

Re: Latency. Please share experiences.

I think that anyone choosing to write directly to any broker's API is going to send their order on the tick that satisfies their chosen set of conditions rather than wait to send it on the following tick - as Multicharts does with Buy/Sell Next bar orders and IOG set.Hi Gerler that is pretty amazing time saving - any chance you can share your methodology Thanks.

How much of a time difference is there between the two? It depends when the next tick arrives. Until it arrives, your order isn't sent. So, anywhere from sub microsecond to ????

During slow periods, I've seen orders not appear on the book for well over a second. For FIFO markets, that is always going to mean that your order will be much further down the queue than it would have been if the order had been sent immediately.

-

TJ

- Posts: 7752

- Joined: 29 Aug 2006

- Location: Global Citizen

- Has thanked: 1033 times

- Been thanked: 2228 times

Re: Latency. Please share experiences.

For slow markets, you should always deploy RecalcLastBarAfter.I think that anyone choosing to write directly to any broker's API is going to send their order on the tick that satisfies their chosen set of conditions rather than wait to send it on the following tick - as Multicharts does with Buy/Sell Next bar orders and IOG set.Hi Gerler that is pretty amazing time saving - any chance you can share your methodology Thanks.

How much of a time difference is there between the two? It depends when the next tick arrives. Until it arrives, your order isn't sent. So, anywhere from sub microsecond to ????

During slow periods, I've seen orders not appear on the book for well over a second. For FIFO markets, that is always going to mean that your order will be much further down the queue than it would have been if the order had been sent immediately.

As a matter of fact, for prudent trade management,

one should always deploy RecalcLastBarAfter.

Re: Latency. Please share experiences.

All that does is initialize the calculation after expiration of the timeout and force recalculation. It doesn't ensure that the order will be sent on the tick it was generated.For slow markets, you should always deploy RecalcLastBarAfter.

As a matter of fact, for prudent trade management,

one should always deploy RecalcLastBarAfter.

For 'really' prudent trade management, all orders should be sent to the broker immediately on the tick that they were generated.

-

JoshM

- Posts: 2195

- Joined: 20 May 2011

- Location: The Netherlands

- Has thanked: 1544 times

- Been thanked: 1565 times

- Contact:

Re: Latency. Please share experiences.

I don't think you can submit an order on the tick it was generated, since that tick will trigger the script calculation process and so will always be a 'historical' tick by the time the order is generated by the code.All that does is initialize the calculation after expiration of the timeout and force recalculation. It doesn't ensure that the order will be sent on the tick it was generated.

For 'really' prudent trade management, all orders should be sent to the broker immediately on the tick that they were generated.

With IOG you can send orders for the next tick of which they are triggered on. And for slow markets you can indeed add `RecalcLastBarAfter()`, which will send the order on the next script calculation (so no need to wait for a new tick).

Re: Latency. Please share experiences.

Thanks JoshM, I think you are correct but that restriction is ONLY due to MC's built-in design of 'Buy Next Bar' which in effect becomes 'Buy Next Tick' when IOG is on.I don't think you can submit an order on the tick it was generated, since that tick will trigger the script calculation process and so will always be a 'historical' tick by the time the order is generated by the code.

Regarding the historical nature of ticks: The second tick also has to be received before the order generated by the first tick is sent. So in that sense, it too is 'historical' by the time it is received.

Receiving a tick is just like any other 'event' that triggers an action (e.g. Print, Write to a File, Send an SMS etc. Those processes don't have to wait for the next tick to be actioned).

I see no reason why the same tick satisfying a set of trade condition(s) can't also call the broker's API to place a trade without having to wait for another tick. Why design a process flow that has to wait for the next tick when it isn't necessary? It kinda violates the K.I.S.S. principle that is often preached.

e.g. If I create a dll that places trades via the broker's API, and call that instead of MC's 'Buy Next bar', that dll will immediately place the order on the same tick - No?

If I can do that, then Multicharts could do that. It may require the addition of a new instruction e.g. something like: 'Buy/Sell This Bar @ 'xxxx.xx Price' with IOG on - to fit in with the Multicharts process but it isn't impossible.

Re: Latency. Please share experiences.

I am not privy to the internals of MC event handling architecture but I suspect that compatibility with large legacy base of EL was perhaps a consideration. I find MC to be fairly well thought out and well designed. In any case, as you say, it is quite easy to insert your own DLL and call the broker's API if this is a high priority for your strategy. Note that not all strategies care about acting on each tick.I see no reason why the same tick satisfying a set of trade condition(s) can't also call the broker's API to place a trade without having to wait for another tick. Why design a process flow that has to wait for the next tick when it isn't necessary? It kinda violates the K.I.S.S. principle that is often preached.

e.g. If I create a dll that places trades via the broker's API, and call that instead of MC's 'Buy Next bar', that dll will immediately place the order on the same tick - No?

Re: Latency. Please share experiences.

I think you're correct in saying that this results from an old architecture that was originally conceived out of necessity and to overcome limitations a long time ago.I am not privy to the internals of MC event handling architecture but I suspect that compatibility with large legacy base of EL was perhaps a consideration.

e.g. EL pre-IntrabarPersist comes to mind as a possible reason for a now, very inefficient design that requires repeated sending of the same order on every tick but there may be other, legacy related reasons.

To be fair to MC, I don't think the design of the (at least) one tick lag and order 'loop' where it is mandatory to resend the same order(s) on every single tick is MC's. It was Omega Research's and MC would have had to follow suit if it wanted to be compatible with TS. It may well have been well thought out when it was first conceived, as a workaround to various constraints - but it isn't necessary now and it is an incredibly inefficient and dated process design. So to still describe such an inefficient process flow as 'well designed' is extremely generous IMO.I find MC to be fairly well thought out and well designed.

Yes, it should be relatively easy to insert a dll that only places an order once and then only resends an order to modify if/when conditions change - even more so for MC as position monitoring is already integrated - which is why it is strange that they haven't done it.In any case, as you say, it is quite easy to insert your own DLL and call the broker's API if this is a high priority for your strategy. Note that not all strategies care about acting on each tick.

That is correct but every strategy will be impacted to some extent regarding the queue position of its orders that result from them being held back by (at least) one tick.Note that not all strategies care about acting on each tick.

As I'm sure you know, a lot of orders can be sent in one tick and that could represent 100's of positions lower in the queue - even if your datafeed provides your script with every tick.

Plus, it has knock-on effects which result in other problems which would otherwise not occur - but that's a whole other story.

Re: Latency. Please share experiences.

The flow is what it is perhaps because of legacy compatibility. I am not referring to the flow and semantics of EL/PL as well designed. I am referring to MC platform design which gives you a broker neutral and datafeed neutral platform that allows portfolio trading for a large symbol universe. MC does all that while maintaining compatibility with EL. My benchmarks on MC and TS show that MC executes PL code 5-10X faster than TS executes identical code. That says something about the quality of the design.It may well have been well thought out when it was first conceived, as a workaround to various constraints - but it isn't necessary now and it is an incredibly inefficient and dated process design. So to still describe such an inefficient process flow as 'well designed' is extremely generous IMO.

I don't agree with this. I know of plenty of strategies where even 500ms latency does not matter; leave alone a single tick. That is not to say that there aren't strategies where latency is critical. By the way, I implemented a standalone IB client in C++ to measure latency and it was over 500ms between dispatch of the order in my code and receipt of the execution report from IB. That is not including the latency in receiving the data for placing the order.Every strategy will be impacted to some extent regarding the queue position of its orders that result from them being held back by (at least) one tick. As I'm sure you know, a lot of orders can be sent in one tick and that could represent 100's of positions lower in the queue - even if your datafeed provides your script with every tick. Plus, it has knock-on effects which result in other problems which would otherwise not occur - but that's a whole other story.

Re: Latency. Please share experiences.

Yes, I think we already agreed on that but we no longer live in the world that made those legacy inefficiencies necessary.The flow is what it is perhaps because of legacy compatibility.

You may not be but I am. The topic of the thread is 'Latency' - not broker and datafeed compatibility (which, BTW I also think is a fantastic feature in MC). I'm just addressing the original question and pointing out that there is a latency that has been deliberately built-in by design.I am not referring to the flow and semantics of EL/PL as well designed.

I've never conducted such a test so I'll have to take your word for it - but 5-10X faster?? Even if that's correct, maybe it just says more about the even worse quality of the TS design.My benchmarks on MC and TS show that MC executes PL code 5-10X faster than TS executes identical code. That says something about the quality of the design.

That kind of benchmarking, which focuses on speed of code execution, only tests the ability of your machine and the software on it to crunch that code. It does not address 'latency' of order submission which is what this thread was discussing.

Yes, so do I. There are many strategies that are profitable regardless of latency - so I agree if you mean: 'does not matter' in the sense of: 'still profitable'. However, unless you've never missed a move because your Limit order wasn't filled, how could you possibly know how many orders would have been filled if you had joined the queue one (or more) ticks ago - and then quantify that impact on the strategy's profitability over the course of a year?I know of plenty of strategies where even 500ms latency does not matter; leave alone a single tick.

I wouldn't underestimate the value of a tick. e.g. If a one tick delay was universally enforced, the entire HFT industry would shut down overnight.

But you don't have to be involved with HFT to be impacted by inefficient design. All large moves begin with a single tick. You're either on those moves or not. I see no reason to increase the likelihoood of missing those moves (and/or optimal exits) due to a legacy design when it is avoidable.

Re: Latency. Please share experiences.

In my assessment, there are too many other things missing with my platform (MC), my datafeed, and my broker for this this single tick delay to matter. But since you seem to believe otherwise, perhaps you can do a forward test of your strategies running inside MC. You will need two MC licenses running side by side with one placing orders with MC and thus incurring the tick delay and the other bypassing the MC tick delay and placing orders via your DLL. You will need a minimum of three months of such forward testing to give you a sound statistical basis for such a belief. When done with the experiment, please post your results on this forum.I wouldn't underestimate the value of a tick. e.g. If a one tick delay was universally enforced, the entire HFT industry would shut down overnight. But you don't have to be involved with HFT to be impacted by inefficient design. All large moves begin with a single tick.

Re: Latency. Please share experiences.

I've placed the order from MC the exact moment when a tick came in that satisfied my conditions. I've achieved this with 2 different methods:

1. by using a 1 tick chart

2. by placing the order via a custom dll

1. by using a 1 tick chart

2. by placing the order via a custom dll

For slow markets, you should always deploy RecalcLastBarAfter.I think that anyone choosing to write directly to any broker's API is going to send their order on the tick that satisfies their chosen set of conditions rather than wait to send it on the following tick - as Multicharts does with Buy/Sell Next bar orders and IOG set.Hi Gerler that is pretty amazing time saving - any chance you can share your methodology Thanks.

How much of a time difference is there between the two? It depends when the next tick arrives. Until it arrives, your order isn't sent. So, anywhere from sub microsecond to ????

During slow periods, I've seen orders not appear on the book for well over a second. For FIFO markets, that is always going to mean that your order will be much further down the queue than it would have been if the order had been sent immediately.

As a matter of fact, for prudent trade management,

one should always deploy RecalcLastBarAfter.

Re: Latency. Please share experiences.